When Netflix walked away from a bidding showdown for Warner Bros. Discovery at the end of February, its stock popped and Wall Street analysts lauded the streaming giant’s financial discipline. Then it received a $2.8 billion break-up fee from Paramount and further boosted its financial outlook with a late March price hike in the U.S. for new sign-ups. Now what?

Netflix co-CEO Ted Sarandos recently described Warner Bros. as a special opportunity that nevertheless wasn’t worth overpaying for and traveled to Europe for an international charm offensive in a signal that the streamer had indeed moved on.

This week, Netflix unveiled a bigger play for young audiences with the launch of a games app for kids, the renewal of two preschool series and a new show based on one of the most enduring nursery rhymes of all time.

Now, after this flurry of activity, Wall Street is gearing up for Netflix’s first earnings update since the end of the WBD auction. Among other things, analysts will listen on April 16 for any insight on management’s plans for how to invest the break-up fee, the impact of latest price increases and whether the forecast for strong growth in advertising revenue this year is on track.

“We go back to the focus on the stock before the Warner Bros. deal, which was a few things,” John Belton, portfolio manager of Gabelli Funds’ Gabelli Growth Innovators ETF, tells The Hollywood Reporter. “Number one was the engagement trends. Investors are going to be focused on that metric and trends there, given engagement is really the lifeblood of the company and is really what fuels the long-term revenue and earnings growth.”

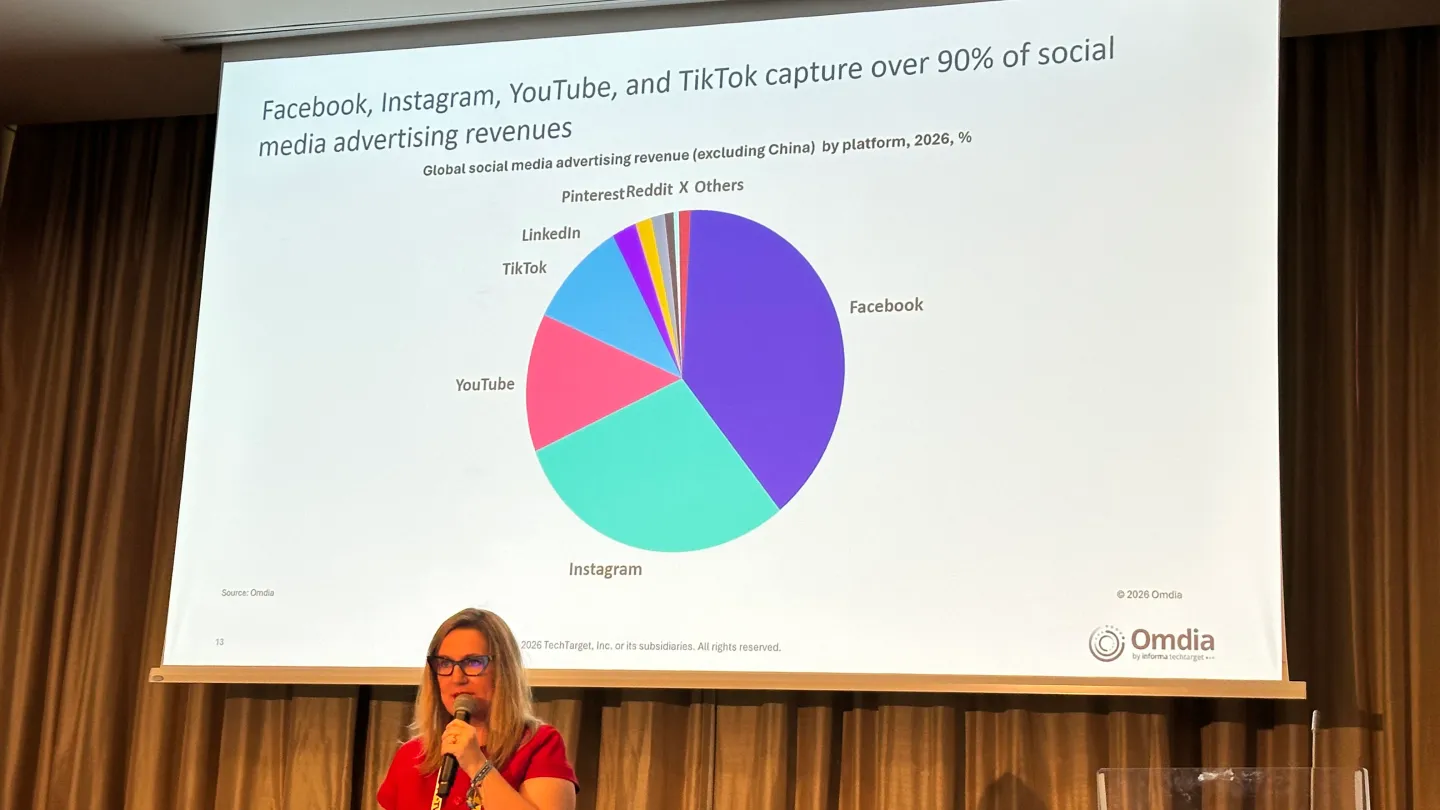

Second is the ad business. “The ad business is really starting to scale into a nice, high-margin, multi-billion-dollar revenue business,” Belton says. “I think we’re entering another phase for the ad business, where they are becoming one of the largest scaled global advertising platforms. Improvements in things like ad formats, ad tech, targeting, and personalization – that’s all going to be in focus. The third thing is there’s just been a recent price increase in the U.S., so it’s going to be focused on early observations around customer response to that.”

Finally, Belton is keeping an eye on the longer-term content spending trend. “Now that the Warner Bros. deal is done, what’s the shape of content spending over the next couple of years?” he says. “They’ve signaled content expense is going to re-accelerate slightly this year. They’ve also, at the same time, suggested that they’re nowhere near peak margins yet.”

Similar themes made their way into stock analysts’ Netflix earnings previews. Below, THR has compiled some of the projections for Netflix’s first-quarter 2026 earnings report and the related management call.

Analyst: Jessica Reif Ehrlich, Bank of America Securities

Stock rating and price target: buy, $125

Takeaways: In a recent report, the expert said it was “back to business” for the streaming giant. After all, “first-quarter results represent Netflix’s first earnings call following the decision to walk away from the WBD acquisition, and we expect management to address this decision head-on.”

But Reif Ehrlich doesn’t expect smooth sailing. “We see several crosswinds to Netflix’s share performance near term,” she highlighted. “On one hand, amid an uncertain macro environment, Netflix appears defensive given their sticky subscriber revenue. On the other, concerns related to engagement trends and AI are currently difficult to disprove.”

The analyst also weighed in on the U.S. price increases under the headline “streamflation,” offering: “While a price increase was expected (implicit in revenue guide for calendar year 2026), the timing appears earlier than the market anticipated. Given the overarching concerns regarding engagement over the last 12-18 months, we view these increases as a validator of Netflix’s confidence in their underlying strength and durability. This reinforces our view of management’s ability to drive average revenue per user (ARPU) growth even at a significantly larger global scale.”

Explaining her “buy” rating, she noted: “Netflix shares will be fueled by continued positive subscriber and earnings momentum in addition to a long runway for advertising and live opportunities. Supported by its world-class brand, leading global subscriber scale, position as an innovator and increased visibility in growth drivers, we believe that Netflix’s shares will perform well.”

Analyst: Alicia Reese, Wedbush Securities

Stock rating and price target: outperform, $118, up from $115

Takeaways: “Netflix is positioning for substantial growth in global advertising, while its latest price increases could provide a meaningful boost to profitability this year,” Reese wrote in a bullish preview note. “We expect domestic resilience, but European resistance to price increases could be an overhang this year as Netflix works through legal challenges.”

That was a reference to a Rome court’s recent finding that Netflix illegally issued price increases from 2017 to 2024 by changing the terms of its subscription without sufficient notice and reasoning. The ruling came amid similar lawsuits across the European Union, including ones filed in Germany, the Netherlands and Poland.

“Should Netflix overcome European challenges to its subscription price increases, we could see further upside in its share price this year,” the analyst highlighted. “We remain positive on Netflix’s overall opportunity to expand revenue in 2026 on both domestic subscription pricing and advertising revenue, while continuing to expand its global footprint.”

Reese forecast first-quarter revenue of $12.22 billion, compared with the Wall Street consensus of $12.18 billion and guidance of $12.16 billion, and earnings per share of 77 cents, compared with the consensus and guidance of 76 cents. She also mentioned Netflix’s “incremental $2.8 billion to spend on content and ad stack improvements this year from its WB deal break-up fee, which we expect to extend its competitive lead.”

Analyst: Sean Diffley, Morgan Stanley

Stock rating and price target: overweight, $115, up from $110 previously

Takeaways: “Reclaiming the Crown” was the headline Diffley chose as he assumed lead coverage of Netflix for the firm, reiterated an “overweight” rating and boosted the price target by $5. “Netflix without Warner Bros. is a cleaner, higher-visibility, and lower-volatility business with more degrees of freedom and lower financial leverage,” he concluded. “The multiple should re-rate back to more than 30x as revenue growth trumps hours and AI flips from risk to opportunity.”

Engagement concerns were also a focus for him. “Sentiment on the pace of engagement growth and margin expansion look to have bottomed,” the analyst suggested, forecasting sustainable double-digit revenue growth ahead. While planned investments will slow the pace of profit margin expansion this year, he underlined his belief in the firm’s pricing power and operating leverage.

Overall, the expert’s view is that the stock is “too cheap” relative to the business’ growth momentum and durability. In fact, he highlighted that in the past, one of the best times to own Netflix shares has been following announcements of U.S. price increases. He cited an average return of 20 percent in the subsequent nine months when analyzing price hikes since 2015.

Diffley also mentioned Netflix’s recent deal for Ben Affleck’s AI company InterPositive. “Netflix can flip the script and move into the AI winner category starting with InterPositive driving significant cost savings and expanding what is possible creatively,” he concluded.

Analyst: Daniel Kurnos, Benchmark

Stock rating and price target: hold, no price target

Takeaways: Kurnos has maintained his “hold” rating on the streaming stock heading into the earnings report. “We have seen Wall Street by and large gushing over the recent price hikes (unexpected only from a timing and sizing perspective), and with good reason: even after shaving off 10 million net adds from our forecast due to the expected impact from elevated pricing and churn, we still ended up with an incremental 100 basis points of revenue growth and slightly more than that in incremental operating margin dollars,” he wrote.

“And the impact is not just limited to ’26; we are now even more substantially ahead of the Street on ’27 revenue and operating income, including the potential for yet another pricing tweak later next year,” he continued. “We now anticipate that Netflix could grow revenue at a mid-teens rate over at least the medium term.”

However, “that is only half the story,” the analyst emphasized with words of caution: “The only time in recent history Netflix raised pricing during a tough macro was in ’22, and subs missed expectations (to be fair, between the COVID pull forward and multiple other competitor pushes and lack of an AVOD offering, this is a tenuous data point).”

But he also argued that in terms of content strategy, “Netflix is clearly undergoing a strategic pivot away from quantity, their differentiating factor, to quality, with the latter a much more expensive strategy.” Tied to that, the analyst suggested that “all eyes will remain on any color around engagement – there is a reason we just went through this whole M&A saga, and nothing has materially changed since investors first began showing concern.”

Analyst: John Blackledge, TD Cowen

Stock rating and price target: buy, $112

Takeaways: “We expect paid net adds of 4.56 million, reflecting seasonality and strong slate of originals, including Bridgerton season 4 and The Night Agent season 3,” the analyst wrote. “The first quarter should also benefit from Stranger Things finale viewership.”

Blackledge also noted that Netflix shares are up 9 percent year-to-date, compared with the close to flat S&P 500 stock index. Noted the expert: “Shares have rebounded sharply following management’s Feb. 26 decision to walk away from the WB deal.”

Addressing the U.S. price hike, for the Standard With Ads tier from $7.99 to $8.99, the Standard plan from $17.99 to $19.99, and the Premium plan from $24.99 to $26.99, Blackledge highlighted that they amount to an 11 percent increase on average.

“We estimate U.S./Canada average revenue per member (ARM) rises 6 percent year-over-year in ’26,” he concluded. “These increases could flow through to existing users in the coming months.”

Analyst: Mark Mahaney, Evercore ISI

Stock rating and price target: outperform, $115

Takeaways: Calling first-quarter Street estimates “highly reasonable, the expert looked ahead to the current second quarter, sharing: “Netflix is likely to benefit from a continuing strong content slate and its very recently announced U.S. price increase. We also view the Street’s second-quarter operating income as achievable given historical seasonality and guidance.”

For all of 2026, Mahaney expects Netflix to “either maintain or modestly raise its guidance of revenue, operating margin and free cash flow.”

He even suggested: “In terms of likely stock reaction, we would assume that Netflix would trade off modestly were the company to not increase its 2026 guidance.”

About the price hike in the U.S., the analyst said: “At comparable price tiers, Netflix remains largely in line to slightly above peers, but with a differentiated content and scale advantage. In the $8-$12 range, ad-supported offerings from Disney+ (~$11.99), Peacock (~$8) and Paramount+ (~$9) compete closely, while Amazon Prime Video (~$9 with ads) comes slightly below. In the mid-tier (~$15–$18), Netflix’s new Standard price sits above Disney+ (~$15.99 ad-free) but remains comparable to HBO Max and Hulu (~$16–$18). At the premium end (~$20–$25), the Netflix Premium tier falls at the high end of the market, where HBO Max ($23) and other bundled offerings (Disney+ bundle at $30) also cluster, suggesting limited pricing dislocation despite headline increases.”

Analyst: Brian Pitz, BMO Equity Research

Stock rating and price target: outperform, $135

Takeaways: Pitz recently reiterated his “outperform” rating, citing the stock’s “cleaner story post-WBD.”

Addressing the price hikes, he offered: “While we suspect recent U.S. price increases were likely embedded in initial 2026 guidance, we raise our 2026 revenue estimate by 0.9 percent to $51.6 billion to reflect higher U.S. prices.”

Pitz also detailed some math. “We estimate recent U.S. price increases should contribute around $1.5 billion in incremental revenue in 2026, providing 3.3 percent growth from pricing alone, as bears question the durability of pricing power amid slowing engagement growth,” he wrote.

All in all, he concluded: “Shares remain attractive …, with likely upside to estimates as we see a clearer story post the WBD acquisition break.” Explained Pitz: “We see a cleaner Netflix story post-WBD merger break, as investors refocus around core/near-term fundamentals and seek evidence that Netflix can scale a massive $10 billion-plus advertising business over the long term.”